As we count down the last few weeks of 2023, your “To Do” list is probably full of holiday shopping and events. Before the new year sneaks up on you, consider taking a little bit of time to evaluate if you need to cross a few things off of your financial to-do list, especially those items that can have an impact on your 2023 income tax return. If you hold traditional IRA assets, a Roth conversion is one of those items.

Roth IRAs offer tax-free benefits in retirement, when certain conditions are met, in addition to tax-deferred accumulations. Anyone can choose to convert existing traditional IRA assets to a Roth IRA, but conversion comes with a cost—you pay income taxes on the amount you convert in the calendar year you convert. Therefore, it is important to review your situation with your tax professional before year end to see if a Roth conversion strategy is right for you.

Why would you consider a Roth conversion? Conversion can be advantageous if you think you will be in the same or higher income tax bracket in retirement and you:

As we count down the last few weeks of 2023, your “To Do” list is probably full of holiday shopping and events. Before the new year sneaks up on you, consider taking a little bit of time to evaluate if you need to cross a few things off of your financial to-do list, especially those items that can have an impact on your 2023 income tax return. If you hold traditional IRA assets, a Roth conversion is one of those items.

Roth IRAs offer tax-free benefits in retirement, when certain conditions are met, in addition to tax-deferred accumulations. Anyone can choose to convert existing traditional IRA assets to a Roth IRA, but conversion comes with a cost—you pay income taxes on the amount you convert in the calendar year you convert. Therefore, it is important to review your situation with your tax professional before year end to see if a Roth conversion strategy is right for you.

Why would you consider a Roth conversion? Conversion can be advantageous if you think you will be in the same or higher income tax bracket in retirement and you:

- Desire tax-free retirement income (after five years and age 59 ½), or wish to create more choice and tax efficiency by deciding which retirement assets you choose to draw retirement income from

- Want to reduce or possibly eliminate required minimum distributions during your lifetime

- Desire tax-free income for your heirs after your death

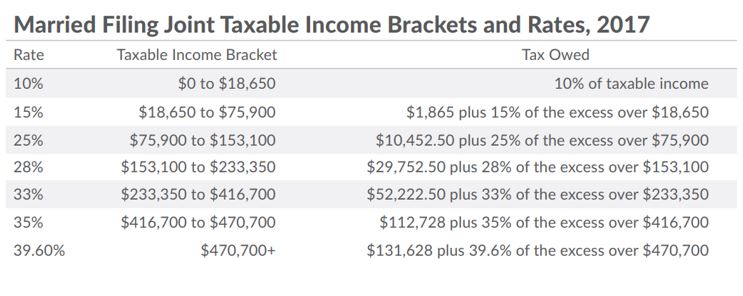

Additional tax-policy changes could take place over the next few years that might alter the course of the current sunsetting rates. Since there are a few years until that would happen, converting systematically to a Roth IRA over the next few years will allow you to lock in today’s lower income tax rates and better manage the additional taxable income that results from the annual conversions.

Back-Door Roth Conversions

Another conversion strategy that could warrant a review before the end of the year is a back-door Roth conversion. For higher-income individuals, who have no other IRAs and are ineligible to make annual Roth IRA contributions, it enables the funding of a Roth IRA while limiting the cost of the conversion. It involves making nondeductible (after-tax) contributions to a traditional IRA and then immediately converting to a Roth IRA. The tax cost for the conversion is then limited to the amount earned in the traditional IRA between the date of the contribution and conversion. However, if you have existing IRA balances, special income tax-rules apply when you contribute after-tax dollars, making the benefits of a back-door Roth conversion less desirable.

Funding a Roth IRA through the “back door” can be beneficial not only because it gives higher-income individuals the ability to utilize Roth IRAs to save when their income would otherwise prevent it, but also because it starts the five-year holding period for future tax-free distribution of earnings after age 59½. This is particularly helpful if you have been contributing to a designated Roth account in your 401(k), 403(b) or 457(b) where there are no income limits that prevent your contributions. At your retirement or separation from service, balances in a Roth 401(k) would be eligible for rollover to a Roth IRA. Because those rollovers don’t carry the holding period from the plan into the Roth IRA, rolling into a pre-existing Roth IRA means your five-year holding period has already begun and you are not starting over with having to satisfy the five-year rule.

Conversion is not right for everyone, and you should review your individual circumstances with a tax professional prior to making a decision to convert because once you convert, you cannot undo it. Talk to your Benjamin F. Edwards financial advisor if you would like additional information about Roth conversions.

IMPORTANT DISCLOSURES: The information provided is based on internal and external sources that are considered reliable; however, the accuracy of this information is not guaranteed. This piece is intended to provide accurate information regarding the subject matter discussed. It is made available with the understanding that Benjamin F. Edwards is not engaged in rendering legal, accounting or tax preparation services. Specific questions on taxes or legal matters as they relate to your individual situation should be directed to your tax or legal professional.

_________________________________________________

[i] Source: The Tax Foundation, 2017 Tax Brackets | Center for Federal Tax Policy | Tax Foundation

Additional tax-policy changes could take place over the next few years that might alter the course of the current sunsetting rates. Since there are a few years until that would happen, converting systematically to a Roth IRA over the next few years will allow you to lock in today’s lower income tax rates and better manage the additional taxable income that results from the annual conversions.

Back-Door Roth Conversions

Another conversion strategy that could warrant a review before the end of the year is a back-door Roth conversion. For higher-income individuals, who have no other IRAs and are ineligible to make annual Roth IRA contributions, it enables the funding of a Roth IRA while limiting the cost of the conversion. It involves making nondeductible (after-tax) contributions to a traditional IRA and then immediately converting to a Roth IRA. The tax cost for the conversion is then limited to the amount earned in the traditional IRA between the date of the contribution and conversion. However, if you have existing IRA balances, special income tax-rules apply when you contribute after-tax dollars, making the benefits of a back-door Roth conversion less desirable.

Funding a Roth IRA through the “back door” can be beneficial not only because it gives higher-income individuals the ability to utilize Roth IRAs to save when their income would otherwise prevent it, but also because it starts the five-year holding period for future tax-free distribution of earnings after age 59½. This is particularly helpful if you have been contributing to a designated Roth account in your 401(k), 403(b) or 457(b) where there are no income limits that prevent your contributions. At your retirement or separation from service, balances in a Roth 401(k) would be eligible for rollover to a Roth IRA. Because those rollovers don’t carry the holding period from the plan into the Roth IRA, rolling into a pre-existing Roth IRA means your five-year holding period has already begun and you are not starting over with having to satisfy the five-year rule.

Conversion is not right for everyone, and you should review your individual circumstances with a tax professional prior to making a decision to convert because once you convert, you cannot undo it. Talk to your Benjamin F. Edwards financial advisor if you would like additional information about Roth conversions.

IMPORTANT DISCLOSURES: The information provided is based on internal and external sources that are considered reliable; however, the accuracy of this information is not guaranteed. This piece is intended to provide accurate information regarding the subject matter discussed. It is made available with the understanding that Benjamin F. Edwards is not engaged in rendering legal, accounting or tax preparation services. Specific questions on taxes or legal matters as they relate to your individual situation should be directed to your tax or legal professional.

_________________________________________________

[i] Source: The Tax Foundation, 2017 Tax Brackets | Center for Federal Tax Policy | Tax Foundation